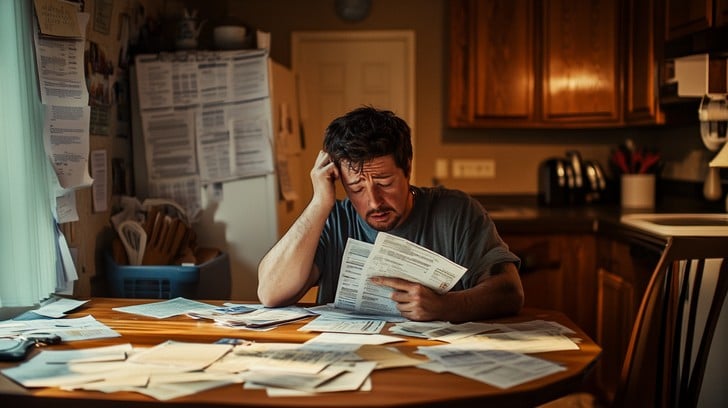

Can Bankruptcy Stop Foreclosure? — Learn Your Options

Bankruptcy can create an immediate pause (an automatic stay) on foreclosure — giving you time to explore modifications, repayment plans, or a controlled exit. Get a free consultation with a Georgia specialist who can explain whether bankruptcy could help your situation.

CALL TODAY !

(470) 516-2603

Can Bankruptcy Stop My Foreclosure?

Yes — in many cases. When you file for bankruptcy, the court issues an automatic stay that immediately halts most collection actions, including foreclosure sales and sheriff auctions. That pause gives you breathing room to evaluate permanent solutions.

But: Bankruptcy is a legal process with long-term consequences — it’s not right for everyone. Read on to understand how Chapter 7 and Chapter 13 work, what each can and cannot do, and how they fit into preforeclosure strategies in Georgia.

Chapter 7 vs Chapter 13 — Which Helps Prevent Foreclosure?

Chapter 7 Bankruptcy (Liquidation)

What it does:

- Eliminates many unsecured debts (credit cards, medical bills).

- Trustee may sell nonexempt assets to repay creditors.

How it may affect your mortgage:

- Chapter 7 does not eliminate secured debts simply by filing. If you want to keep the home and you’re behind on mortgage payments, Chapter 7 alone usually won’t stop foreclosure unless you immediately catch up on payments or negotiate with the lender.

- If you cannot keep the home, Chapter 7 may let you walk away with fewer unsecured debts, but the lender can still foreclose unless you negotiate or file another protective measure.

Good for:

- Homeowners who don’t plan to keep the house and need a fresh start on unsecured debt.

Chapter 13 Bankruptcy (Reorganization) —

The most powerful tool to stop foreclosure

What it does:

- Creates a court-approved repayment plan (typically 3–5 years) to catch up on missed mortgage payments while keeping the home.

- The automatic stay prevents foreclosure while your Chapter 13 plan is in place.

How it helps with preforeclosure:

- Stops foreclosure sales and sheriff auctions while you reorganize.

- You can pay past-due amounts over time through the Chapter 13 plan rather than in a lump sum.

- In many cases, interest and fees may be restructured in the plan.

Good for:

- Homeowners who can realistically afford a restructured payment plan and want to keep the home.

NEED HELP? CALL TODAY (470) 516-2603

Pros & Cons: Be Informed

Pros

Cons

Immediate halt to foreclosure actions (automatic stay).

Time to reorganize finances and negotiate with lenders.

Chapter 13 can allow you to catch up on missed mortgage payments over time.

May stop deficiency judgments depending on how the case and state law interact.

Can provide a structured plan and peace of mind.

Bankruptcy appears on credit reports (Chapter 7 or 13) and has long-term credit effects.

Chapter 7 may not prevent foreclosure if you can’t reinstate or redeem the mortgage.

Costs: attorney fees, filing fees, trustee payments (varies).

Potentially losing non-exempt assets (Chapter 7).

Complex legal paperwork — mistakes can be costly.

How Do We Help You

We’re not attorneys — but we help by:

- Explaining how bankruptcy interacts with foreclosure timelines.

- Referring you to experienced Georgia bankruptcy attorneys.

- Coordinating with attorneys if selling the property during or after bankruptcy is the best option.

- Providing cash-offer or short-sale pathways if bankruptcy doesn’t align with your goals.

Contact / Free Consultation

Get Immediate Help — Free Bankruptcy & Preforeclosure Review

Important: This page provides general information about bankruptcy and preforeclosure options in Georgia. This is not legal advice. Bankruptcy law is complex and fact-specific. Always consult a licensed Georgia bankruptcy attorney before taking any legal action. Property Jet can help connect you with qualified local attorneys.

Bankruptcy FAQ for Preforeclosure

Q: Will filing bankruptcy stop eviction immediately?

Filing triggers an automatic stay that usually stops eviction and auction procedures while the stay is in effect. However, if eviction follows a prior judgment or other special circumstances, consult an attorney.

Q: How will bankruptcy affect my credit?

Both Chapter 7 and 13 can remain on your credit report for 7–10 years. But stopping foreclosure or avoiding it altogether can protect your long-term financial future better than a completed foreclosure in many cases.

Q: How much does bankruptcy cost?

Costs vary by attorney and case complexity. Expect filing fees, attorney fees, and possible trustee or plan payments in Chapter 13.

Quick links

Home

About Us

Property Type

Services

FAQ

Testimonal

Blogs

Popular house

Penthouses

Villa

Smart home

Apartments

Office

Bungalow

LEGAL

Terms of use

Privacy policy

Newsletter

Subscribe to Property Jet Real Estate Solutions ’s newsletter for the latest updates, tips, and insights into residential home inspections. Be the first to know about industry trends, expert advice, and exclusive offers to help you make informed property decisions.

© Copyright 2026. Property Jet Real Estate Solutions . All Rights Reserved.